2 Accounting Concepts

2 usable in practical situations. The concept of materiality is an important issue for auditors of financial accounts.

Lesson 2 Accounting Concept And Convention Part 2 Business Entity Conc Lesson Concept Sample Paper

2 CON2 Status Page Qualitative Characteristics of Accounting Information May 1980 Financial Accounting Standards Board of the Financial Accounting Foundation 401 MERRITT 7 PO.

2 accounting concepts. Chapter 2 Managerial Accounting and Cost Concepts Solutions to Questions. BOX 5116 NORWALK CONNECTICUT 06856-5116. This concept assumes that the business will operate for a long period of time and will not be dissolved in the near future.

The concept provides the basis for the formation of the accounting equation. Business Entity Money Measurement Going Concern Accounting Period Cost Concept Duality Aspect concept Realisation Concept Accrual Concept and Matching Concept. The Accounting Concepts.

21 MEANING OF ACCOUNTING CONCEPT Let us take an example. Accounting concepts and convention 1. 26 Solved Scanner CMA Foundation Paper - 2 New Syllabus 11.

In other words if the firm sold everything it had it would be obliged to distribute all. حسام ابو عرجة. The proprietor has no intention to.

Four important accounting concepts underpin the preparation of any set of accounts. Accountants assume unless there is evidence to the contrary that a. 21 accounting concepts Accounting Concepts refer to the basic assumptions rules and principles which work as the basis of recording of business transactions and preparing accounts.

Explain the term accounting concept and explain the meaning and significance of various accounting concepts. Let us go through each one of them briefly. Basic Accounting Concept 2 The business firm is a separate entity distinct from the owners.

The accounting concepts are the rules that are applied in recording transactions and preparing the Trading and Profit and Loss account and the Balance sheet. A firm while it has legal control over items of value it is not the ultimate owner of those things. This concept assumes that business shall continue for an indefinite period.

Accounting concepts and conventions 2. Accountants record increases in asset and expense accounts on the debit left side and they record increases in liability income and equity accounts on the credit right side. In traditional double-entry accounting the left column in the register is used for debits while the right column is used for credits.

According to this concept the business and the owner of the business are two different entities. Accounting principles are accepted as such if they are 1 objective. 4 feasible they can be applied without incurring high costs.

This rule states that only the transactions of the business should be recorded and NOT the owners private transactions. While the expenses are recognized whenever the assets are consumed. These basic accounting concepts are as follows.

In this concept only the revenue is recognized when there is a reasonable certainty that it needs to be realized. And 5 comprehensible to those with a basic knowledge of finance. ACCOUNTING CONCEPTS Business entity concept Money measurement concept Going concern concept Accounting period concept Accounting cost concept Dual aspect concept Matching concept Realisation concept Accrual concept 3.

Business Entity Concept. In other words I and my business are separate. INTRODUCTION Actually there are a number of accounting concepts and principles based on which we prepare our accounts These generally accepted accounting principles lay down accepted assumptions and guidelines and are commonly referred to as accounting concepts 2.

The first two accounting concepts namely Business Entity Concept and Money Measurement Concept are the fundamental concepts of accounting. This concept discusses the issue of the realization of profit. Financial Accounting Concepts No.

Going Concern Concept It is on this concept that a clear distinction made between assets and expenditure. View 2 - Accounting Concepts and Principlespdf from IE 415 at Cebu Technological University formerly Cebu State College of Science and Technology. This concept refuses allocation of cost on different accounting periods.

Accounting principles involve both accounting concepts and accounting conventions. Here the revenue is recognized whenever it is earned.

Book Keeping And Basic Accounting Accounting Principles Budgeting Process Accounting

Topic 2 Accounting Concepts What Is The Accounting Entity Concept Accounting Entity Concept Each Business Is A Accounting Services Accounting Financial

Accounting Class Help Com Accounting Classes Accounting Principles Accounting Education

Accounting Principles Accounting Principles Accounting Jobs Accounting Education

Chapter 2 Accounting Concepts Interactive Worksheet In 2021 Worksheets Interactive Workbook

Schaum S Outline Of Principles Of Accounting I Fifth Edition Schaum S Outlines By Joel Lerner Mcgraw Hill Education Financial Management Advanced Mathematics Business And Economics

Pin On Accounting

Auditing Tax Accounting Concepts Accounting Concept Accounting Logo

Accounting Principles Accounting Principles Accounting Jobs Accounting Education

Accounting Concepts Applications Bookkeeping Business Small Business Bookkeeping Accounting And Finance

Accounting Concepts Principlesofaccounts Tuition Financial Information Revision Notes

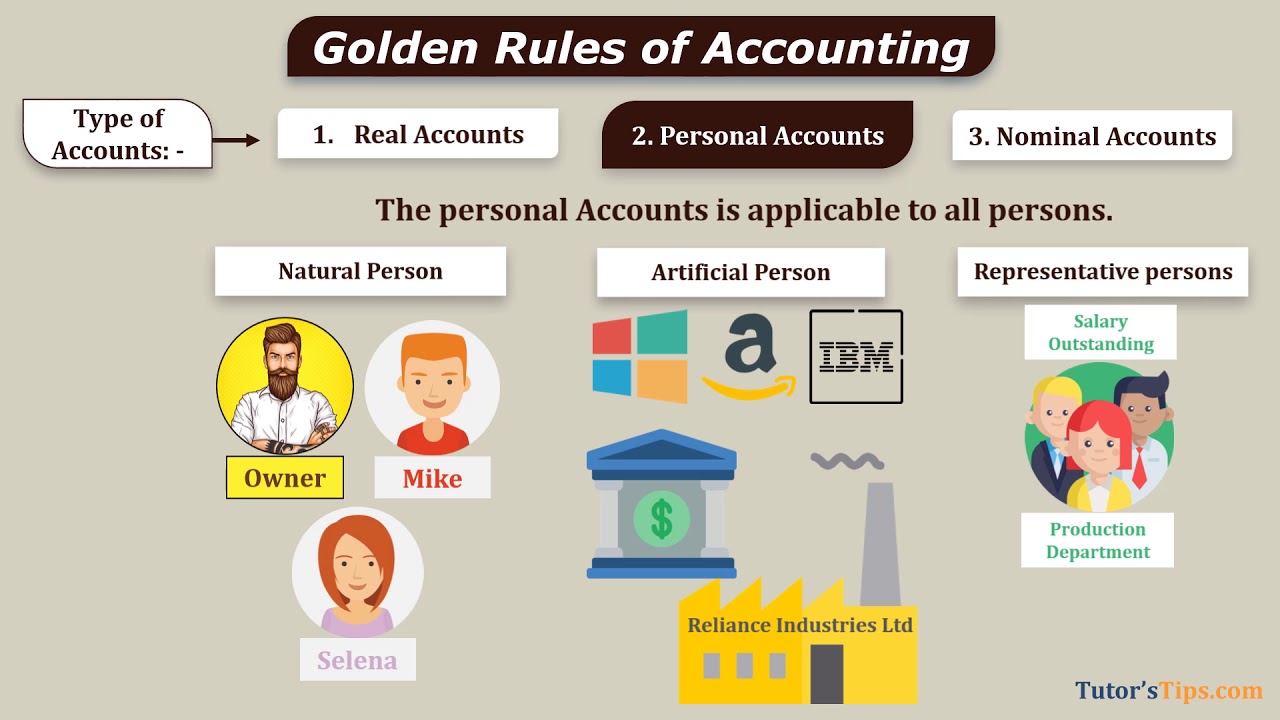

Golden Rules Of Accounting Explain With Animated Examples Tutorstips Learn Accounting Accounting Golden Rule

Bookkeeping And Accounting Visual Accounting Cycle Akuntansi

Pin By Mckell Kimball On The Accountant In Me Conceptual Framework Leadership Management Accounting And Finance

{kind=link}

Posting Komentar untuk "2 Accounting Concepts"